Payroll

Quebec Payroll: RL-1, QPP, QPIP Compliance Guide

Quebec payroll compliance guide covering QPP, QPIP, RL-1 slips, CNESST, Revenu Quebec remittances, and Bill 96. Updated for 2026 with rates and deadlines.

Qpp contribution rate 2026

Workzoom covers qpp contribution rate 2026 as part of the same platform that runs Quebec payroll, rl-1 slip filing, and bill 96 payroll requirements: on one employee record, with statutory rates maintained in the platform.

Most multi-province employers don't run into trouble in Quebec because the rules are hard. They run into trouble because they assumed Quebec was a setting, not a second payroll.

Here's what most payroll teams miss. It's not a configuration change. It's a parallel compliance system. Add a British Columbia employee and you change a tax rate and a WCB account. Add a Quebec employee and you change the pension plan, add a deduction, reduce the EI rate, register with a second agency, file a second year-end slip, and potentially translate every pay stub into French.

Quebec payroll is not a regional variation of Canadian payroll. It is a separate compliance regime with its own pension plan, its own parental insurance program, its own tax slips, its own remittance agency, and its own penalties. Employers who treat it as "Ontario payroll with a few tweaks" end up filing corrections, paying penalties, or both.

If you have even one employee working in Quebec, you are subject to Revenu Québec rules, CNESST obligations, and the Quebec Labour Standards Act. This guide covers everything that differs from the rest of Canada, with current 2026 rates. One rule worth keeping: in Quebec, two agencies, two slips, two deadlines.

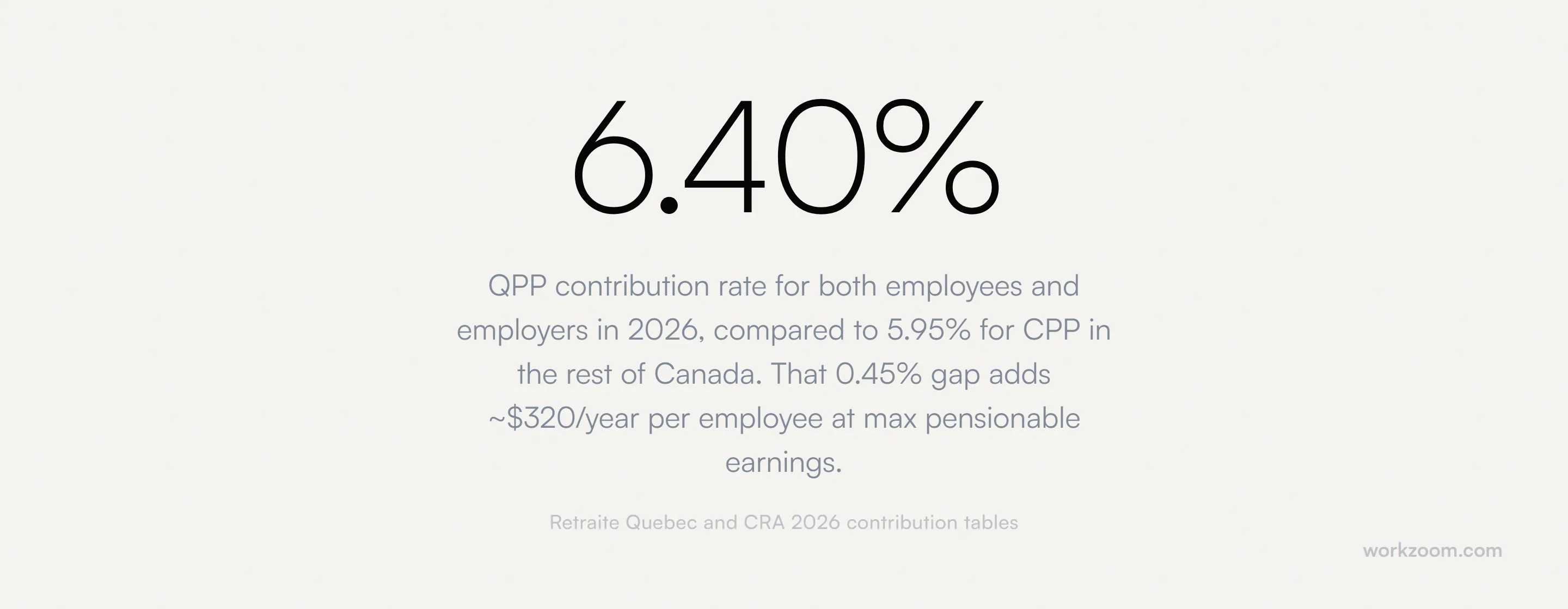

- Quebec employees contribute to QPP (5.3% base + 1% first additional) instead of CPP (5.95%), with separate remittance to Retraite Québec

- QPIP (Quebec Parental Insurance Plan) replaces the parental portion of EI, requiring separate deductions and remittances

- You must file RL-1 slips with Revenu Québec AND T4 slips with CRA. Two agencies, two deadlines, two penalty regimes

- CNESST (workers' comp) premiums are employer-paid and based on industry classification

- Bill 96 requires French-language workplace communications for companies with 25+ employees

- Quebec overtime starts at 40 hours/week, not 44 like Ontario

QPP vs CPP: Quebec's Higher Pension Contribution

The most immediate difference for any multi-province employer is the pension plan. Quebec employees do not contribute to the Canada Pension Plan. They contribute to the Quebec Pension Plan (QPP), administered by Retraite Québec.

The QPP rate is higher than CPP. In 2026, the numbers look like this:

| Detail | CPP (Rest of Canada) | QPP (Quebec) |

|---|---|---|

| Base employee rate | 5.95% | 5.3% |

| Base employer rate | 5.95% | 5.3% |

| First additional rate (employee/employer) | 1% / 1% | 1% / 1% |

| Maximum pensionable earnings | $74,600 | $74,600 |

| Basic exemption | $3,500 | $3,500 |

| Maximum annual employee base contribution | $4,230.45 | $3,768.30 |

In 2026, the QPP base rate (5.3%) is actually lower than CPP (5.95%), but the first additional QPP contribution (1%) brings the combined rate to 6.3% — slightly higher than CPP overall. The key cost driver is the separate remittance system and the second additional QPP tier (4% employee + 4% employer on earnings between $74,600 and $85,000), which mirrors the CPP2 structure. A payroll system that conflates QPP with CPP will miscalculate both tiers.

A second additional QPP tier also applies in Quebec, mirroring CPP2. The ceiling is the same ($85,000) and the rate is 4% employee + 4% employer on earnings between $74,600 and $85,000 — but the base QPP calculation underneath uses QPP rates, not CPP. Your payroll system needs to handle both tiers independently for Quebec employees, and a stale second ceiling is exactly the kind of CPP2 misconfiguration that under-deducts all year without anyone noticing.

You cannot simply swap "CPP" for "QPP" in your system. The rates differ, the contribution maximums differ, and the remittance goes to a different agency. A payroll system that treats Quebec as a CPP variant will produce wrong deductions from the first pay run.

QPIP: The Plan That Replaces Part of EI

Quebec employees do not pay into the parental benefits portion of Employment Insurance. Instead, they pay into the Quebec Parental Insurance Plan (QPIP), which covers maternity, paternity, parental, and adoption benefits.

This creates a double calculation problem. Quebec employees pay a reduced EI rate (because parental benefits are carved out) plus a separate QPIP premium. Here are the 2026 rates:

| Plan | Employee Rate | Employer Rate | Maximum Insurable Earnings |

|---|---|---|---|

| EI (rest of Canada) | 1.63% | 2.282% | $68,900 |

| EI (Quebec, reduced) | 1.30% | 1.82% | $68,900 |

| QPIP | 0.430% | 0.602% | $103,000 |

Notice that QPIP has its own maximum insurable earnings ($103,000 in 2026), which is higher than the EI ceiling. This means a Quebec employee earning $90,000 has stopped contributing to EI but is still contributing to QPIP. Your payroll system must track both ceilings independently.

QPIP premiums are remitted to Revenu Québec, not to CRA. This is a separate payment from your federal EI remittance.

Two Agencies, Two Remittances, Two Sets of Penalties

This is the part that catches every multi-province employer the first time. When you have Quebec employees, you remit to two separate agencies:

- CRA: Federal income tax, EI premiums (at the reduced Quebec rate)

- Revenu Québec: Quebec provincial income tax, QPP contributions, QPIP premiums, Quebec Health Services Fund (QHSF)

Each agency has its own remittance schedule, its own account number, its own payment portal, and its own penalty structure. Missing a CRA deadline does not affect your Revenu Québec standing, and vice versa. But missing either one triggers penalties independently.

Revenu Québec's remittance thresholds also differ from CRA's. Your company might be a monthly remitter with CRA but an accelerated remitter with Revenu Québec, depending on your Quebec-specific payroll volume. The two schedules are calculated independently.

RL-1 Slips: Quebec's Version of the T4

At year-end, Quebec employers must file RL-1 slips with Revenu Québec for every employee who worked in the province. This is in addition to the T4 slips you file with CRA.

The RL-1 and T4 are not the same form with a different name. The RL-1 has different boxes, different codes, and different reporting requirements. Some amounts that appear on the T4 don't appear on the RL-1, and vice versa. For example:

- QPP contributions appear on the RL-1, not CPP

- QPIP premiums appear on the RL-1 (no equivalent box on the T4)

- Quebec provincial tax withheld appears on the RL-1

- Private health plan contributions have specific RL-1 box codes that differ from T4 treatment

Both slips are due by the last day of February. Filing one on time but missing the other still results in penalties from the agency you missed.

Your payroll system must generate both T4 and RL-1 slips for Quebec employees. If your system only generates T4s and expects you to manually create RL-1s, you are one missed February deadline away from Revenu Québec penalties.

CNESST: Quebec's Workers' Compensation

Every other province has its own workers' compensation board (WSIB in Ontario, WorkSafeBC in B.C.). Quebec has CNESST (Commission des normes, de l'équité, de la santé et de la sécurité du travail).

CNESST premiums are 100% employer-paid. The rate depends on your industry classification and your company's claims history. Rates can range from under $1.00 per $100 of insurable payroll for low-risk office work to over $10.00 per $100 for high-risk industries like forestry or mining.

CNESST also enforces workplace safety standards in Quebec, which means your compliance obligations go beyond just paying premiums. You must maintain a prevention program, report workplace accidents within 24 hours, and accommodate injured workers according to Quebec-specific rules.

For multi-province employers, CNESST coverage applies to employees who work in Quebec, regardless of where your company is headquartered. You need a separate CNESST account and separate premium payments from whatever you pay WSIB or WCB in other provinces.

Quebec Labour Standards: What Differs From Ontario

The Quebec Labour Standards Act (Loi sur les normes du travail) creates different rules than Ontario's Employment Standards Act. If your HR policies are built for Ontario, they will be non-compliant in Quebec on several fronts.

Overtime Threshold

Quebec overtime kicks in at 40 hours per week. Ontario's threshold is 44 hours. For an employee working 42 hours in a week, Quebec owes overtime. Ontario does not. If your time tracking system uses a single overtime threshold across all provinces, you are either overpaying Ontario employees or underpaying Quebec employees.

Statutory Holidays

Quebec recognises 8 statutory holidays, and the list differs from Ontario's. Quebec includes Saint-Jean-Baptiste Day (June 24) and the National Day for Truth and Reconciliation. Ontario includes Family Day (third Monday of February), which Quebec does not observe. Your holiday pay calculations must be province-specific.

Leave Entitlements

Quebec provides different leave rules than the rest of Canada:

- Vacation: 3 weeks after 3 years of service (Ontario requires 3 weeks after 5 years)

- Family obligations leave: Up to 10 days per year (first 2 paid after 3 months of service)

- Domestic violence leave: Up to 26 weeks unpaid, plus 2 days paid

- Bereavement: 5 days (2 paid) for immediate family, compared to Ontario's 2 unpaid days

These are minimums under Quebec law. Your employee handbook must reflect Quebec-specific entitlements if you have staff in the province. A single Canada-wide policy will be non-compliant in at least one jurisdiction.

Bill 96: French Language Requirements

Bill 96 (An Act respecting French, the official and common language of Québec) expanded language requirements significantly starting in 2022, with phased implementation continuing through 2026.

For employers with 25 or more employees in Quebec (lowered from 50), Bill 96 requires:

- French as the language of workplace communication, including internal memos, policies, and software interfaces

- Employment contracts offered in French first (employees can request English, but the French version governs in case of dispute)

- Job postings in French (other languages permitted only if French is included)

- Registration with the Office québécois de la langue française (OQLF) and implementation of a francisation program

For HR and payroll specifically, this means pay stubs, T4/RL-1 correspondence, benefits enrolment materials, and workplace policies must be available in French. If your HR software only outputs English documents, you have a compliance gap.

Bill 96 applies to companies with 25+ employees in Quebec, not 25+ employees total. If you have 500 employees across Canada but only 30 in Quebec, you are still subject to francisation requirements for your Quebec operations.

Quebec Health Services Fund (QHSF)

Ontario has the Employer Health Tax. Quebec has the Health Services Fund (Fonds des services de santé). The rate depends on your total payroll and whether you're in the primary or manufacturing sector.

For most employers with total payroll over $7 million, the QHSF rate is 4.26% of Quebec payroll. Smaller employers pay graduated rates starting at 1.65%. This is a significant cost that does not exist in several other provinces (Alberta, for example, has no employer health tax at all).

QHSF is remitted to Revenu Québec along with your QPP and QPIP payments. It is calculated on your total Quebec payroll, not per employee.

Why Multi-Province Employers Get Tripped Up

The problem is not that Quebec rules are complicated. Every province has its own quirks. The problem is that Quebec's differences are systemic, not incremental.

An employer adding a British Columbia employee to an Ontario-based payroll needs to change the provincial tax rate and WCB account. The CPP, EI, and year-end filing process stays the same.

An employer adding a Quebec employee needs to change the pension plan (QPP instead of CPP), add a new deduction (QPIP), reduce the EI rate, register with a second remittance agency (Revenu Québec), file a second year-end slip (RL-1), register with CNESST, apply different overtime thresholds, observe different statutory holidays, offer different leave entitlements, and potentially comply with French language requirements.

That is not a configuration change. That is a parallel compliance system running alongside your existing one. The pattern we see across Canadian payroll clients is that the first Quebec hire is where a single-province payroll setup quietly stops being trustworthy: the math still runs, but it runs on the wrong assumptions.

You got into payroll to pay people correctly, not to keep a second rulebook in your head and hope you remembered the overtime threshold. When a Quebec deduction comes out wrong, it's not your fault: it's a system that was only ever taught one province.

What Your Payroll System Needs for Quebec

If you are evaluating payroll software and you have employees in Quebec (or plan to), here is the minimum your system must support natively:

- QPP calculations at the correct 5.3% base + 1% first additional rate, separate from CPP

- QPIP deductions with Quebec's separate maximum insurable earnings ($103,000)

- Reduced Quebec EI rate (1.30% employee, 1.82% employer)

- Dual remittance to both CRA and Revenu Québec, with independent schedules

- RL-1 slip generation alongside T4s, with correct box mapping

- CNESST premium tracking by industry classification

- QHSF calculation based on total Quebec payroll

- Quebec-specific overtime at 40 hours (not 44)

- Quebec statutory holidays including Saint-Jean-Baptiste Day

- Quebec leave entitlements that differ from your other provincial policies

- French-language pay stubs and documents for Bill 96 compliance

If your current system requires manual workarounds for more than two of those items, you are carrying compliance risk that scales with every Quebec employee you add.

Quebec payroll, handled natively

Workzoom calculates QPP, QPIP, CNESST, and QHSF automatically. RL-1 slips generate alongside T4s. Dual remittance to CRA and Revenu Québec, tracked independently. $4/employee/month per suite, no setup fees, no contracts, month-to-month.

Book a 15-Minute WalkthroughGetting Started: Registration Checklist

If you are about to hire your first Quebec employee, here is what you need to register for before that first pay run:

- Revenu Québec account: Register for source deductions (QPP, QPIP, provincial tax, QHSF). This is separate from your CRA business number.

- CNESST registration: Required before the employee's first day. Premiums are based on your industry classification.

- OQLF registration (if 25+ Quebec employees): Required within 6 months of reaching the threshold. You must submit a francisation analysis.

- Quebec payroll configuration: Update your payroll system to apply QPP rates, QPIP deductions, reduced EI, and Quebec provincial tax tables.

- Policy review: Ensure your employee handbook covers Quebec-specific leave entitlements, overtime thresholds, and statutory holidays.

Missing any of these creates liability from day one. Revenu Québec penalties for failure to register can reach $2,500 per occurrence, and CNESST can impose fines for unregistered employers that exceed $10,000.

Quebec payroll compliance is not something you figure out after hiring. You need Revenu Québec and CNESST registrations before your first Quebec employee's first paycheque. Retroactive registration does not waive the penalties for the period you were unregistered. For the federal side of the same year-end, see our Canadian payroll deductions guide.

See Workzoom in 30 minutes.

Real product, real questions, no slides. Starts at $4 per employee per month, CAD or USD, with $0 setup fees.

What readers ask after this post on Quebec payroll.

Live on Workzoom right now. North America and the Caribbean.

Workzoom handles HR, payroll, workforce, and talent on one employee record. Book a 30-minute walkthrough.

Related reads

View all in Payroll